What's Really Driving No-Fault Premiums

Seemingly every year the topic of reforming Michigan's unique no-fault automobile insurance system comes up. The approaches to reform are varied, but the primary cause for conversation has remained the same: some drivers around the state pay as much as $3,000-5,000 a year for their auto insurance.

"Just look at Ohio," some will say. "They only pay $900 on average."

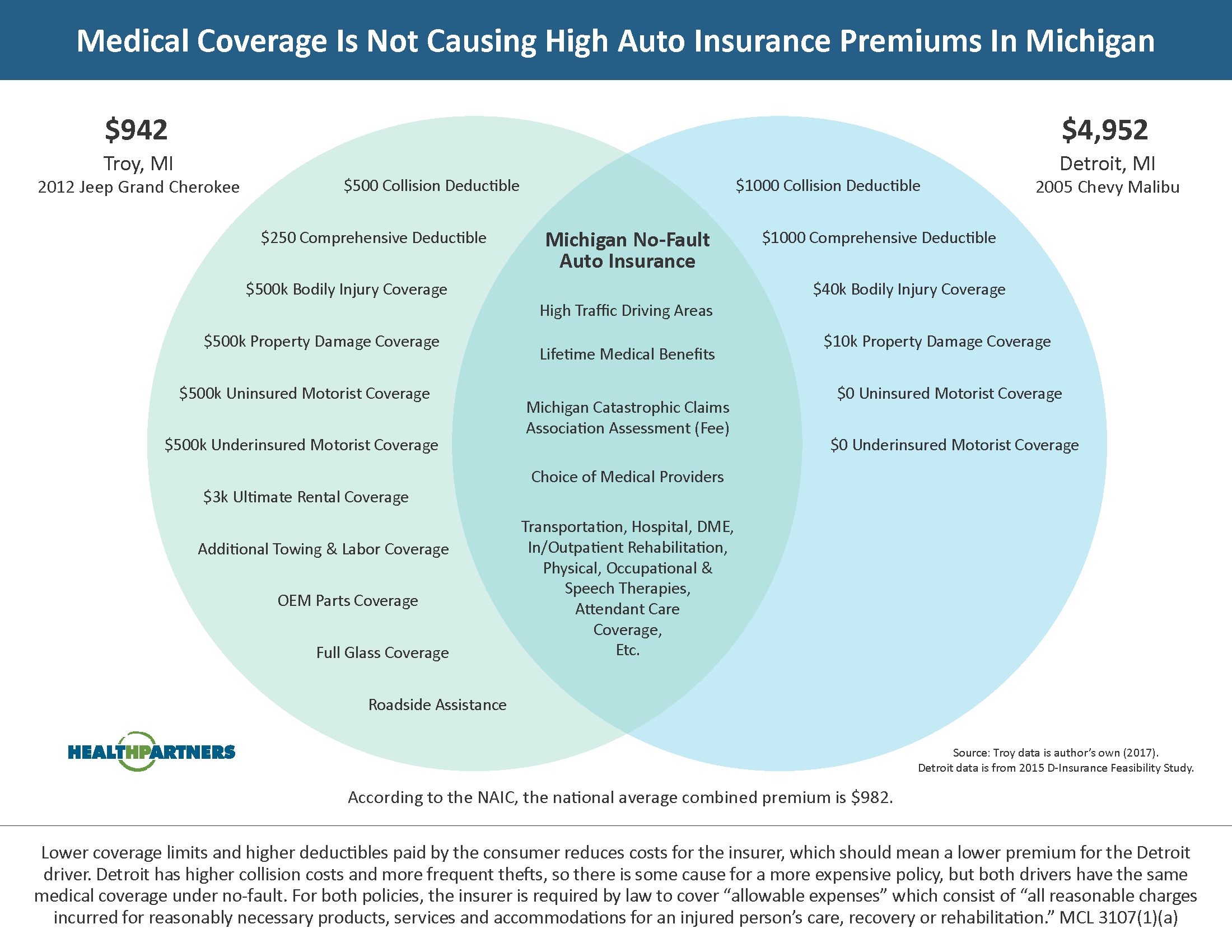

According to the most recent report from the National Association of Insurance Commissioners (NAIC) published January 2017, the national average for auto insurance, regardless of what it covers or how it operates, is $982 per vehicle.

In the 38 states that operate on a tort system, your insurance will pay to repair your car, the damage you cause with it, and give you some protection in the case that you cause an accident, are sued, and owe another driver damages. In tort states you also have to wait for your lawsuit to resolve before you really can start therapy, unless you have enough savings to pay out of pocket.

In 12 other states there is some form of no-fault coverage, where drivers are able to file claims against their own insurance policy, but 11 of those states have caps on that coverage. New Jersey has the second highest coverage limit, with $250,000 in coverage, while Michigan leads the pack with no predetermined limit.

If you've read the news lately, you're probably expecting me to tell you that my premium, because I live in Michigan and have "unlimited" medical benefits, is some disturbing multiple of that $982 national average. Well, I'm here to bring a little light to the issue and break that narrative.

My Michigan no-fault auto insurance premium comes in at $942, with full medical coverage and increased limits for bodily injury, property damage, and uninsured/underinsured motorist coverages. I'm young, male, and live in the largest city in Oakland County, a suburb of Detroit.

How can my insurance be $40 less than the national average if I live in the dreaded state of Michigan and have lifetime medical benefits, you might ask. Everything you've heard on this topic has told you that my premium should be at least a few thousand bucks. I mean I do have to pay for unlimited healthcare for my negligent neighbors, right?

What if that narrative is wrong? What if a lack of regulation on insurers allows them to include all sorts of unscrupulous factors such as zip code (redlining), credit scores, and occupation? What if no-fault and it's extensive medical benefits aren't the problem, and the issue truly lies in the hands of insurance providers?

Consumer Protections Needed

Factory workers are being charged more than lawyers for their auto insurance policies even if they drive the same car, both have perfect driving records, and they live the same zip code, according to a new study. The study reveals that insurers are using non-driving related factors such as occupation, level of education, and home ownership status to set rates, and that these factors can increase a driver's premium by as much as 18%.

"State law requires that Michigan drivers buy auto insurance, but it doesn't protect blue collar workers and out-of-work residents from abusive pricing practices by insurance companies," said Doug Heller, who authored the study. "Pricing people based on their job-type or education or home ownership not only has nothing to do with their safety on the roads, it makes it harder for financially-strapped drivers to maintain their coverage."

A follow up study showed that some insurance companies in Michigan charge women up to 38% more than men for the same policy.

There are 31 practices specifically prohibited by the Michigan Consumer Protection Act, one of which reads "Charging the consumer a price grossly in excess of the price at which similar property or services are sold." However, Michigan insurance companies are immune to this act due to a series of court decisions that essentially rendered all regulated businesses exempt.

Even the Insurance Commissioner (now known as the Director of the Department of Insurance and Financial Services) lacks the ability to come in and say rates are too high. Technically, it is true that the director would be able to find rates to be excessive; however, they essentially have to prove the unprovable. In order to find the rates excessive, the director would need to prove that "the rate is unreasonably high for the insurance coverage provided and a reasonable degree of competition does not exist for the insurance" (MCL 500.2109(1)(a)).

Proving there isn't a "reasonable degree of competition" is the difficult part, largely due to the number of insurers that sell in this state. In fact, a 2005 market competition study, initiated by then Insurance Commissioner Linda A. Waters, found "private passenger auto insurance … throughout the state [is] reasonably competitive" and, as such, "the rates charged by private insurers … could not be found to excessive under current law, even if they were found to be unreasonably high in relation to covered losses."

That report went on to say, "It is very clear that in many parts of the state, competition isn't doing enough for consumers. Insurers are not competing in a manner that actually makes insurance more affordable in these areas."

Without a functioning Consumer Protection Act or an empowered, consumer-oriented Insurance Commissioner, Michigan drivers are essentially left to pay whatever their insurance companies charge them. This has often been referred to as "file and use" because insurance companies are able to do just that. For many people, this unchecked "file and use" system is becoming increasingly unaffordable.

Several other states have taken steps to address these issues and it's time for Michigan to do the same.

What Actually Happens In Other States

There's a reason Susan Connors, President of the Brain Injury Association of America, has said "As state governments continue to seek out the best practices across the nation, policymakers would do well to take note of the shining example that is Michigan auto no-fault insurance."

Some of the people recently calling for reforms have cynically asked how other states are able to get by without this coverage. Attorney Tom Sinas was recently interviewed on Know the Law and does a great job explaining this.

"We call it a no-fault system because it's a system that allows you to access benefits without proving the fault of someone else, and that's really unusual," Sinas said. "The old days, and the days that some people say we should go back to, went like this: if you're involved in an automobile accident, in order to claim anything, lost time from work, medical expenses, pain and suffering type damages, you had to prove the fault of the other driver."

This situation can be troublesome for an injured person because research shows prompt treatment can dramatically improve recovery and lawsuits take time.

"What we realized along the way is that was not a very efficient way to run a system where we know we have a lot of auto accidents," Sinas said. "We want to get people access to things like medical care and wage replacement without having to prove a case against someone else. But if we didn't have no-fault, then your ability to get any of those benefits would again require that you pursue a lawsuit against the other driver and prove that that person was at fault."

Even if a person is able to prove fault and win their case, that doesn't mean the other driver can always pay or that the amount won will cover all of their medical bills.

Sinas goes on, "Do you know what the minimum amount of liability coverage in the state of Michigan is? $20,000. So if we didn't have a no-fault system, and you had $100,000 worth of medical bills, well too bad, you're going to be limited to the $20,000 the other driver had. That's the limitation that is imposed by a fault based system."

Without adequate funds from the at-fault driver, the injured person remains on the hook for their outstanding bills, and having quickly used up whatever health insurance coverage they had, turns to Medicare or Medicaid.

"What else does it mean?" asked Sinas. "Well what it means, in that hypothetical, is that your medical bills are not going to be covered by the other driver's insurance company because he's got $20,000 in coverage and you've got $100,000 in medical bills. So who pays those bills? Well the only places to go are health insurance, Medicaid, and Medicare."

Essentially this leads to increased health insurance costs for drivers in those states because they're more likely to use that coverage, and there are also more people signing up to use Medicare and Medicaid. In 2002, Colorado repealed no-fault and just three years later, their Medicaid system had a 205% increase in costs.

Furthermore, private health insurance, Medicare, and Medicaid all provide significantly fewer products and services for injured people, particularly those with brain injuries. "The lack of coverage means that thousands of patients are discharged each year from hospitals to nursing homes or to languish in their beds during the critical early months when their brains are most receptive to healing, according to data from the National Institute for Disability and Rehabilitation Research. At least two-thirds of patients discharged from rehabilitation hospitals after a typical stay of 16 days get no further treatment, the studies indicate. Without intensive therapy, Manley says, brain-trauma patients may never regain full use of their limbs, their ability to use language, their emotional balance or their power to think clearly." (USA Today: For Brain Injuries, A Treatment Gap).

High Praise For Michigan's No-Fault System

Michiganders should be grateful that our system helps to contain costs for other healthcare programs such as Medicare and Medicaid, but we really should also be comparing the services it provides. Again, Michigan is the only state in the country that doesn't predetermine coverage limits on an injured person's care, recovery, and rehabilitation.

"The state of rehabilitative care here in Michigan is second to none in the country," said Tom Constand, President of the Brain Injury Association of Michigan. "We had three facilities within 30 minutes of our house. That's not the case in other states."

Because of laws limiting insurance coverage of auto accidents in many other states, a person in need of rehabilitative care may have to drive hours away, and in some cases even across states lines, to find a facility that provides the necessary care.

"For [my son's] care it was three days a week, four hours a day," Constand said. "In any other state, to drive across the state, to accommodate that kind of schedule, is going to completely change your life. We are so fortunate to have this kind of care in Michigan."

He's right. A friend of mine was in a car accident almost twenty years ago and he had to spend a month in the intensive care unit. The bill for that ICU stay was $1.5 million, an amount that would have bankrupted his family. But because he lived in Michigan and had no-fault insurance, his insurer paid that bill. Today he is still recovering, but is leading a happy and productive life thanks to this insurance system that provides a value that no other state has.

Bob Hunter, the Director of Insurance for the Consumer Federation of America has said, "If I was going to be hit by a car and seriously injured, I'd want to be in Michigan."

Legislative Remedy Should Address Other Factors Involved

As this article, part of the Free Press' investigation into the high costs of Michigan no-fault insurance, pointed out, there are several other factors that contribute to a driver's premium. This particular series focuses on costs in Detroit, but several other investigations have revealed very high premiums in other cities around the state. The factors listed that contribute to high premiums are motor vehicle theft, carjackings, crashes & congested roadways, credit scores, a lack of private health insurance, and zip codes.

Many legislative bills have been introduced over the years to address the high price of auto insurance premiums in our state. The bills have been offered by a variety of representatives, democrats and republicans alike, and vary from limiting the criteria an insurer can use to create rates - no more rates based on education level, credit history, or occupation - to granting the Director of Insurance the power to order refunds for overcharges.

A 2015 bill would've make a ticket for anything less than 6 mph over the speed limit not worth any points on the driver's record, as opposed to the current 2 point standard which can raise your premiums as much as 11% according to Insure.com.

Another bill would have prevented insurers from raising rates for drivers who file claims for damage caused by a pothole. As the folks in Lansing continue to struggle to come up with a solution for the roads, many of the potholes are becoming unavoidable, and drivers are bearing the cost through increased premiums.

Sen. Coleman Young II (D-Detroit) had also introduced legislation in the other chamber. His bill, SB 347, would've required a report every two years regarding the competitiveness of auto insurance in the state, under certain conditions would grant the Director of Insurance power to modify the rate approval process, regulate excess profits, establish and require specific rates, and also establish a plan to assist consumers in understanding "how to obtain automobile insurance at the most favorable rates and how to obtain benefits for which they are eligible."

All of these proposals would help consumers, and would come at no cost to their coverage or to the medical providers that serve them. As Sen. Young said during Mayor Duggan's initial hearing in front of the Senate Insurance Committee for his D-Insurance proposal, "There are other solutions that are offered. The question is are they going to be taken up? That's the question."